Primer:

Data Centres

April 2026

Overview

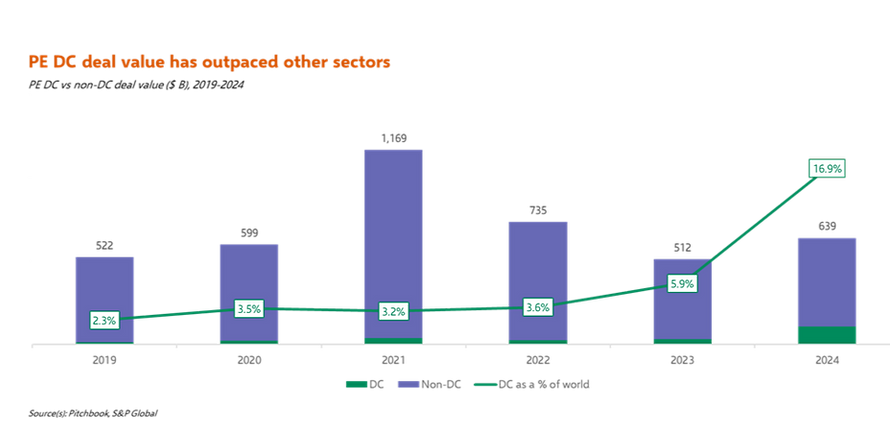

Data Centres (“DC”) are facilities containing servers and network equipment, used to store and manage large amounts of data. Private equity’s (“PE”) presence in DCs has grown significantly, as funds rush to capture a slice of the pie, estimated to be worth $900 billion as of mid-2026. 2024 saw a record $108.1 billion of PE investment into DCs, over 3x as much as in 2023, despite total PE deal value only rising 24.7% year-on-year during the same time frame.

PE’s interest in DCs reflect a dramatic surge in demand for data storage and processing capacity, driven by an increase in the number (quantity) and the complexity (quality) of digital services requested. On the “quantity” front, new innovations become adapted to a variety of use cases as tech companies attempt to solve user pain points. On the “quality” front, new innovations raise people’s expectations for what is possible with technology, resulting in sustained demand for greater efficiency. For instance, researchers found that writers using ChatGPT in 2023 (only months after its initial release) took 40% less time to produce work and their work quality increased by 18%.

In this article, we will explore two aspects of this exciting sector: (i) how PE funds and operators monetise DC assets, and (ii) what the DC PE landscape looks like in Southeast Asia (“SEA”).

1. Monetising DCs

1.1. Types of DC business models

Historically, companies would build enterprise DCs, facilities which are built and owned by companies themselves. However, as companies required increasingly more compute power, it became far too expensive and technically complex to build enterprise DCs.

With the industry reaching a critical mass of companies requiring DCs, two popular DC business models emerged, as follows:

Colocation

Specialised DC developers lease space to companies, providing tenants a secure space to store their hardware. The colocation provider provides all other essential services, such as power, cooling, security and connectivity. Colocation tenants benefit from splitting shared costs of essential services with other tenants, rather than bearing the full costs themselves.

The two types of colocation are as follows:

-

Retail: Companies rent small spaces and individual equipment within the DC. This is suitable for companies which operate smaller-scale operations. Power usage is less intensive, so developers usually charge tenants per rack (a shelf to store DC equipment) used rather than per kilowatt (“kW”) used.

-

Wholesale: Companies rent entire spaces within the DC, suitable for companies which require more space. As power usage is highly intensive, developers charge tenants per kW used. This pricing model generally earns lower margins than retail, because users only pay for the amount of power used (a variable cost), instead of paying for the full rack (a fixed cost).

Hyperscale

Specialised DC developers agree to either (i) lease existing space to a company or (ii) build DCs according to the company’s specifications (termed “build-to-suit partnerships”). Since customisable DCs are highly tailored to the customer’s needs, the developer often transfers ownership to the customer. Customers are typically Big Tech firms whose operations require heavy data load.

Customers’ main customisation needs include optimising power and cooling efficiency according to their hardware. Companies in industries with more advanced security needs may also pursue such partnerships. TikTok has shifted away from colocation to hyperscale in Europe, and is planning to build a €1 billion data centre in Finland, to comply with the European Union’s (“EU”) General Data Protection Regulation (“GDPR”) rules.

Build-to-suit partnerships have become more attractive to investors for the following reasons:

-

Predictable and consistent cash flows: Developers require adequate compensation for the complexity of hyperscale services provided, thus leases often feature long tenures commonly spanning 10-20 years or longer.[5] The predictable cash flows generated de-risks investment into developers and improves their valuations.

-

Sticky demand: Companies which engage build-to-suit services often require standardised DC designs across all DC campuses. Thus, companies engage the same developers across several facilities and geographies to ensure the same DC design is implemented. Developers can generate recurring revenue from servicing the same client. Meta and CoreWeave signed a $21 billion deal running from 2026-2032, to expand Meta’s AI cloud capacity across multiple locations.

Colocation and hyperscale DCs have become more popular over time. The share of enterprise DCs decreased from 56% in 2018 to 32% in 2025, and is projected to decrease further to 19% in 2031. The share of enterprise DCs lost has been mainly replaced by owned hyperscale facilities, suggesting a trend towards complex, highly customised DCs.

1.2. PE investment strategies

PE funds can invest in the DC field on two levels:

-

Asset: The fund acquires a plot of land to operate a DC on it. Such acquisitions and the analysis done closely resemble real estate asset transactions as covered in Part 1. Asset-level transactions can be further broken down into two types:

-

Greenfield: The fund acquires an undeveloped plot of land and builds a new DC on it. Greenfield projects are attractive for build-to-suit partnerships, as starting from scratch allows flexibility and customisation. However, they are typically more expensive, take longer to build, and are usually seen as riskier due to the heightened uncertainty.[1]

-

Brownfield: The fund acquires a developed plot of land. Transactions may include (i) repurposing the existing asset into a DC, (ii) acquiring a DC midway through construction, or (iii) acquiring a fully operational DC. Brownfield projects are cost-effective and can be deployed faster, and are often seen as less risky due to less complications from approval to delivery. However, not every site may be suitable for repurposing.[2]

-

-

Corporate: The fund acquires a stake in an operator who specialises in developing and operating DC assets. The proceeds from the equity raise may be used to fund further asset buildouts. Such acquisitions and the analysis done closely resemble typical leveraged buyouts (“LBO”).

The more mature a market is, the more likely the market can support complex corporate acquisitions, which are only appealing if the operator has a portfolio of attractive DC assets. Less mature markets do not have a critical mass of attractive DC assets, and thus see more asset-level transactions.

2. SEA Market Analysis

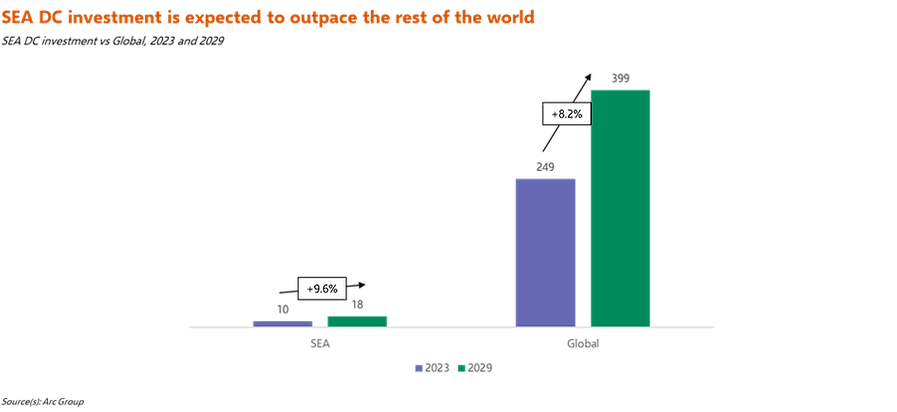

SEA is a nascent but fast-growing DC market, often outpacing developed markets which face labour and power constraints. As of early-2026, SEA has overtaken Northeast Asia and Australia/New Zealand, two major Asia-Pacific (“APAC”) markets, in DC capacity growth and pipeline expansion.[3] From 2023-2029, SEA DC investment is expected to exceed the rest of the world.[4]

2.1. SEA growth drivers

Key growth drivers of the SEA DC market can be separated into demand and supply drivers, as follows:

2.1.1. Demand drivers

Large and growing digital consumer market

Digital penetration rates are higher in SEA than globally, despite SEA’s developing status. SEA is home to nearly 705 million residents, comprising 8.5% of the global population. 500 million of them are internet users, comprising 10% of the global population. Possible reasons are as follows:

-

SEA’s population skews younger: Over 50% of SEA’s population is under the age of 30.[3] Young populations are a common trend in developing countries, driven by lower female education rates, lower life expectancy and family-oriented cultures. SEA’s younger demographic were born and raised in the digital era, reflecting a greater proclivity and savviness towards digital tools.

-

Leapfrog effect: This effect describes the phenomenon where countries which develop later skip stages of development, allowing them to close the development gap with developed countries at a faster rate. SEA was still experiencing rapid development during the popularisation of mass-market technology in the late 2000s-early 2010s, allowing it to integrate advanced features like digital payments and artificial intelligence (“AI”) tools into online services much faster. This effect can also be evidenced by the outsized interest in AI in SEA; SEA consumers exhibit a 3x interest in AI and 1.6x net positive attitudes towards AI than the rest of the world.

Gross Merchandise Value (“GMV”) transacted across digital platforms in the 6 largest SEA economies (“SEA-6”) has exhibited a strong 15% growth rate each year from 2023-2025. Revenue growth in the SEA-6 has also largely mirrored that of GMV, showing that companies have been able to consistently monetise digital interest.[6] This growth presents a compelling value proposition for companies reliant on digital services to expand their presence in SEA, increasing the need for compute power and capacity.

Tighter data protection laws

To protect data from outside interference, SEA countries have increasingly implemented more robust Personal Data Protection (“PDP”) regulations, especially placing greater restrictions on cross-border data transfers. Companies which wish to capture the exciting SEA digital market opportunity must abide by these regulations and may find it easier to construct DC infrastructure within the region.

Examples of recent PDPA developments in SEA include the following:

-

Malaysia: Recent amendments were added to the existing PDP regulations in 2024, mandating that personal data can only be transferred to countries with similar laws or equivalent levels of data protection.

-

Indonesia: Passed its first comprehensive PDP law in 2022, further restricting cross-border data transfers and heavily penalising breaches.

-

Vietnam: A new PDP law took effect in 2026, requiring companies who wish to transfer data abroad to submit a Cross-Border Transfer Impact Assessment (“CBTIA”) to the Ministry of Public Security for approval. The CBTIA would allow the ministry to understand where data is transferred to and the data security standards of the recipient country.

2.1.2. Supply drivers

Favourable CAPEX costs

Excluding Singapore, SEA countries offer 20% lower costs for DC construction per megawatt (“MW”) on average compared to the rest of the world. Many SEA countries have relatively large and under-developed land space which allows for cheaper land acquisition costs. Moreover, rapid urbanisation in SEA has led to strong market competition among contractors leading to price competition.

Favourable OPEX costs

SEA countries are again highly competitive against other major DC markets, at 20-30% lower. With a favourable location for export, many SEA countries aim to attract foreign investment in their industrial sectors and become integrated into global value chains. Thus, many companies in SEA which provide essential inputs are nationalised, so that the government can offer generous subsidies and tax benefits which drive input costs down.

• Labour: Cost of living in SEA is generally lower than developed markets, driving wages down.

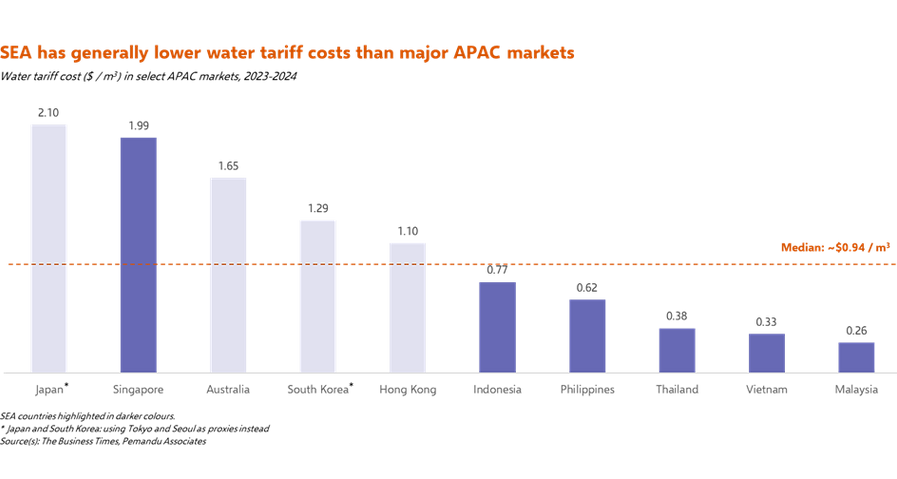

• Water: DCs are extremely water-intensive in order to cool equipment from high heat produced during operations. One hyperscale facility can use up to 1.5 million litres of water a day for cooling, approximately the daily water usage of 15,000 people at 100 litres each. SEA features far lower water tariffs than major APAC markets. ,

• Electricity: Indonesia, Malaysia and Vietnam, the SEA DC markets with the lowest electricity costs, have 40% lower electricity costs than US and 70-80% lower than Australia and Japan.

2.2. Key regional risks

Low electricity grid investment limits DC expansion

DCs are extremely energy-intensive assets. Electricity consumption by DCs has grown 12% per year over the last 5 years, and makes up ~1.5% of global electricity consumption today.[1] The growing demand for electricity in SEA has been met by a consistent growth in low-emissions electricity generation in SEA. Yet, investment into the electricity grids in SEA to transmit and distribute electricity to end users has decreased in the last 10 years. This has created an $18 billion annual investment gap for SEA grid investment, with the gap projected to increase to $29 billion by 2035.

As SEA countries are highly diverse in terms of renewable energy potential and demand, the ASEAN Power Grid (“APG”) was conceptualised in 1997 to connect national grids into a unified regional network. However, the project has been unable to raise the estimated $27 billion of capital needed by 2040, with some of the major issues to do so including:

• Lack of private sector participation: Many SEA countries maintain state control of their grids, as centralised electricity coordination is a key part of their growth trajectories as developing nations. SEA thus struggles to attract private capital and historically has relied on their state-owned enterprises’ (“SOE”) balance sheets, which may be tied up in other investments.

• Domestic borrowing constraints: Most SEA countries impose a 15-25% cap on the amount of capital banks can lend to any one borrower. As most SEA banks are of national importance, the cap exists to reduce concentration risk and encourage financial discipline. Since SOE utilities engage in highly capital-intensive activities, banks regularly approach the cap for lending to them, limiting how much they can borrow for new projects. This problem has been especially observed in Indonesia and Vietnam, where domestic bond markets are under-developed.

• Technical and physical constraints: Much of the grid must be connected by sea as many SEA countries are separated by water. Subsea cables can be easily damaged by (i) natural events, such as seabed movements or strong currents; and (ii) external activities, such as fishing activities. Since SEA is an active region for trade with a high density of maritime traffic, the risk of damage is elevated, and the potential costs are substantial. A section of subsea interconnector between Estonia and Finland damaged by a ship’s anchor cost between €50-60 million to repair, excluding revenue lost during the repair period.

These limitations pose a challenge to investors to commit to SEA. According to a Q1 2026 survey of DC operators and hyperscalers in SEA, grid connection delays (90%) and transmission capacity limits (70%) are the top 2 factors constraining further DC investment in SEA. Moreover, 50% of respondents indicated that >25% of their planned projects depended on grid upgrades that were not yet funded or constructed.

2.3. The SIJORI growth triangle

As a non-mature market, DC development in SEA is heavily fragmented. The regions exhibiting the strongest growth are those which possess compelling demand and supply drivers to support expensive large-scale DC buildout.

One of the key regions that has attracted substantial DC investment is termed the Singapore-Johor-Riau Islands (“SIJORI”) growth triangle. SIJORI is an economic cooperation initiative signed by Singapore, Malaysia and Indonesia in 1994 to enhance economic ties and promote joint growth in the region.[1] In this region, DC acquisition, investment and buildout activity has substantially picked up, with mega deals worth >$1 billion taking place. It currently holds 930MW of live capacity,[2] making up 46% of live capacity in the three countries as of H1 2025.

Singapore

Singapore is by far the largest DC market in SEA, housing nearly 68% of DC capacity, 5x more than its closest competitor Indonesia. Key factors behind its prominence include:

-

Proximity to major markets: Singapore positions itself as the gateway between SEA and the rest of the world, offering low-latency connectivity to markets like Perth, Australia and Chongqing, China. It was the first country to establish point-to-point internet connectivity with China.

-

Stable political climate: Singapore features a long-standing political administration with high efficiency and low corruption, allowing businesses to set up DCs relatively quickly with less unexpected delays

-

No natural disasters: Unpredictable disasters such as cyclones and earthquakes can damage the structural integrity of real assets, increasing risk for investors and operators. Singapore is located away from major tectonic plates (unlike its neighbour Indonesia) and near the equator, where tropical cyclones do not reach.

However, DC growth in Singapore is expected to be the slowest compared to other SEA-6 countries, due to the following factors:

-

Expensive buildout costs: Singapore’s land space is extremely well-developed and limited, driving land prices up. Land costs around $1,700 per m2, resulting in a developer incurring $6.9 million in land costs for an average 10-acre site. As the richest economy in SEA, wages and utility costs are also far higher than what companies can obtain in neighbouring countries.

-

Regulatory restrictions: In 2019, the Singapore government placed a temporary moratorium on DC construction. By 2014, DCs accounted for 7% of Singapore’s electricity consumption, largely powered using natural gas, and the government was concerned that DCs’ explosive growth could result in a spiralling carbon footprint. While the moratorium was lifted in 2022, new DC builds must be approved by the government, based on resource efficiency and their alignment with Singapore’s national objectives. For example, Singapore’s Green DC Roadmap requires new DCs to achieve a Power Usage Effectiveness (“PUE”) of <1.3, the most stringent criteria in APAC.

Due to these disadvantages, recent PE deal activity is largely concentrated around corporate acquisitions of Singapore-headquartered DC operators who are expanding their pipelines in neighbouring regions, such as Johor and the Riau Islands. Both regions have positioned itself as cheaper alternatives in a similar geographical area, while preserving many of the same advantages.

Johor, Malaysia

While Johor currently has much less DC capacity than Singapore, much of its DC capacity is still in the pipeline. It boasts a planned capacity pipeline of 5,700 MW and is projected to host 60% of Malaysia’s total DC capacity by 2030 , indicating strong long-term confidence.

Beyond lower input costs while still maintaining close proximity to Singapore, Johor attracts substantial DC expansion for the following unique reasons:

• Ample water supply: Johor receives 2,681mm of average rainfall per year, which would place it 11th in the world if it was a country. While Singapore also receives high annual rainfall as it is also located near the equator, Johor has far larger natural water basins to store water. For instance, the Johor basin features a catchment area of 2,286km2, over 3x larger than Singapore’s land area and 12% of Johor’s land area. J.P. Morgan has estimated that despite the enormous demand for water by Johor’s new DCs, Johor will be able to support 3x the planned capacity additions out to 2028.

• Abundant land: Despite being 3x larger than Singapore, Johor only has 69% of Singapore’s population, providing ample land space for development. During the earlier stages of Johor’s DC development, as of May 2024, Johor had 13 DCs with a land area of just 0.15 km2, just 0.0008% of Johor’s total land space. Johor’s abundant land space allowed the government to approve more DC projects, reaching 51 after just 18 months as of Nov 2025.

Deal activity in Johor is driven less by corporate acquisitions and rather by PE-backed operators. Vantage Data Centres, a DC operator owned by DigitalBridge and Silver Lake, acquired a 300MW hyperscale campus in 2025, funded by a $1.6 billion investment into its APAC platform by Abu Dhabi Investment Authority (“ADIA”) and an affiliate of Singapore’s Government Investment Corporation (“GIC”). Other PE-backed operators, such as Digital Edge and Princeton Digital Group (both backed by Stonepeak), have committed capital into greenfield builds as part of their plan to expand aggressively in Johor.

Riau Islands, Indonesia

The Riau Islands is a group of islands in Western Indonesia south of Singapore. Batam is its largest city and where most DC development occurs in. Most major DC projects in Indonesia are concentrated in Jakarta, with only an estimated 8MW of DC capacity being live in Batam as of Jul 2025. Compared to Johor, a smaller percentage of capacity is live while a larger percentage is in the pipeline, reflecting a less mature market than Johor yet with a greater potential for an accelerated growth trajectory in the short-to-medium term.

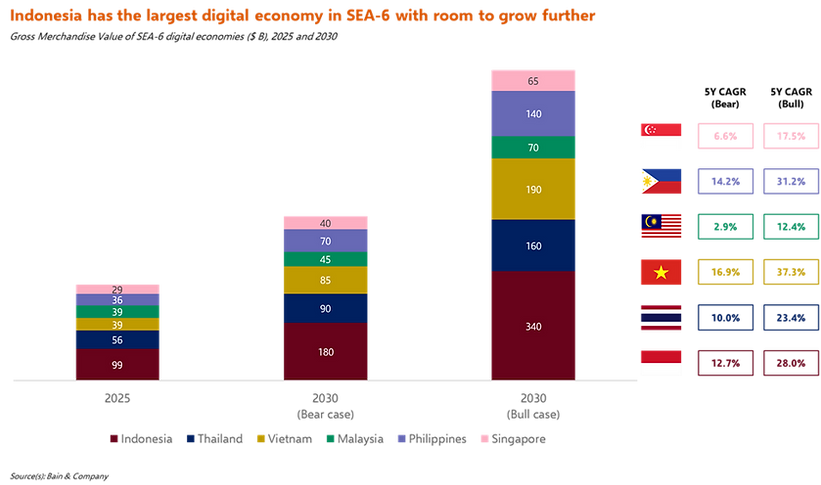

Batam being less mature than Johor stems from it not being as well-endowed with water and land resources. Batam has far less land space than Johor at 1,040km2, which is not much bigger than Singapore. Nevertheless, Batam is attracting notable interest mainly due to significant country-wide demand for digital services. Indonesia has by far the largest population in SEA, and urbanisation driven by the growth of economic hubs in the country has spiked demand for consumer digital services. Thus, it has the largest SEA digital economy, 1.8x larger than its closest rival Thailand. Indonesian digital apps incorporating AI has seen the largest growth in revenue out of all SEA countries from H1 2024 to H1 2025, at 127%. These activities are data-intensive and create demand for DCs. While DCs in Singapore or Johor can serve the Indonesian market, laws regulating cross-border data-sharing (such as Indonesia’s PDP in 2022) makes building DCs in-house more feasible. With land supply in Jakarta rapidly tightening, and with a 1GW IT capacity gap in Indonesia to plug by 2030, Batam is emerging as an alternative entry point for DC operators looking to tap into the lucrative Indonesian digital economy.

Nearly 70% of total IT capacity in Batam is at the “early stage” of development, a stage where the developer has not yet secured all necessary elements to commence the project. Thus, the market is not mature enough to support corporate buyouts or brownfield acquisitions involving PE. Instead, deal activity leans towards developers undertaking greenfield projects, who have to take on substantial risk to break ground. Regional DC operators who know the market more intimately are more willing to take on the risk than large international players. Singapore-headquartered DayOne Data Centres is one of the more established players in Batam, with a 72MW project approved in 2025 and a 500MW hyperscale campus approved in 2026.

Authors:

Vernon Goh

Vansh Goel (Associate AY 25/26)

Jatin Singh Kodial (Associate AY 25/26)

Ishita Gupta (Analyst AY 25/26)

Zhao Junyu (Analyst AY 25/26)